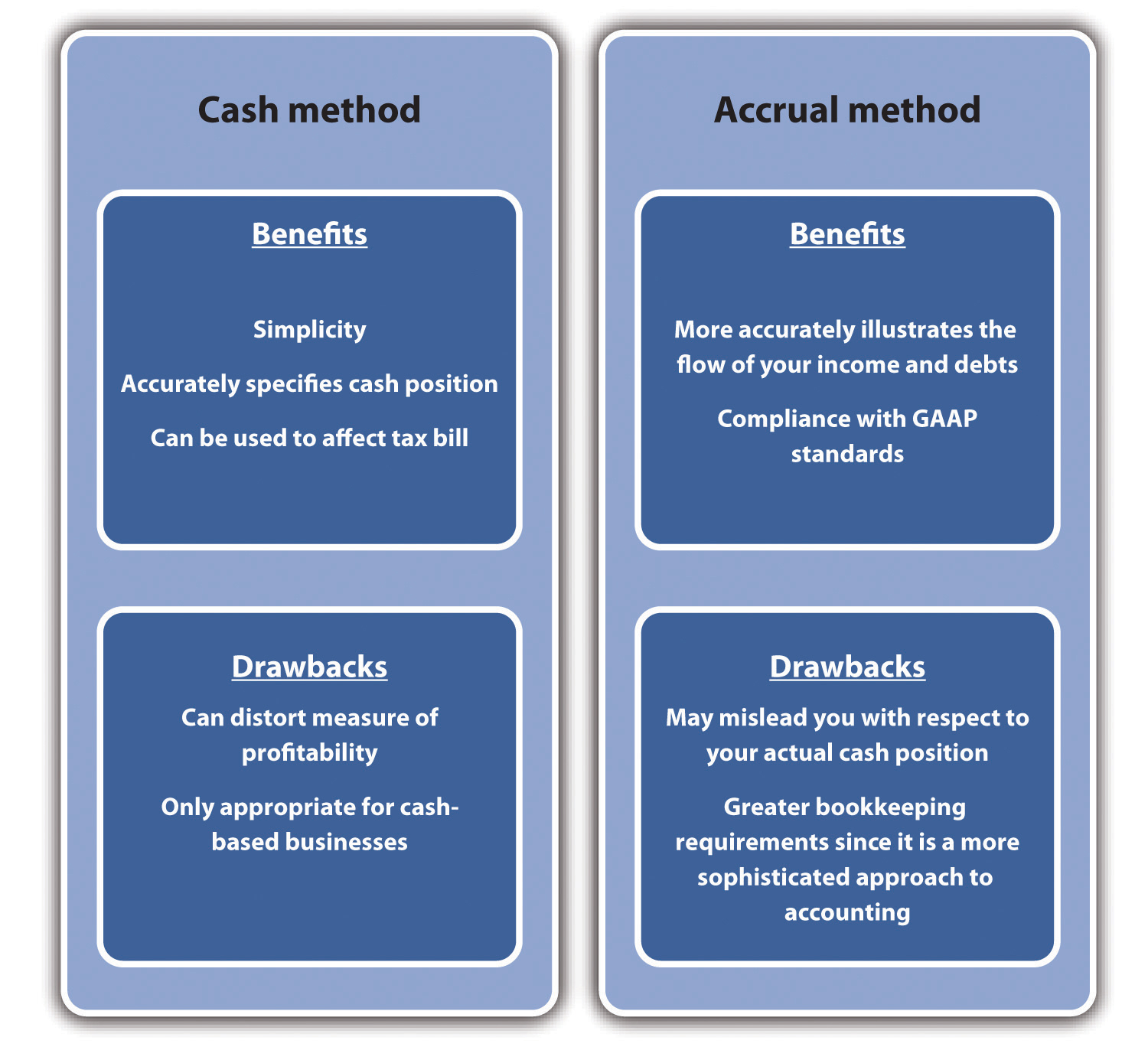

The mercantile system of accounting, also known as the traditional system or the cash basis system, is a method of accounting that focuses on recording financial transactions when they occur, rather than when payment is received or made. This system is based on the idea that businesses should record their income and expenses at the time of sale or purchase, rather than waiting for payment to be received or made.

In the mercantile system, revenue is recorded when it is earned, regardless of when payment is received. Similarly, expenses are recorded when they are incurred, regardless of when payment is made. This approach is in contrast to the accrual basis of accounting, which records revenue and expenses when they are earned or incurred, regardless of when payment is received or made.

The mercantile system has a number of advantages and disadvantages. One of the main advantages is that it is relatively simple to understand and implement, making it well-suited to small businesses with limited resources. It is also relatively easy to reconcile cash inflows and outflows using this system, as all transactions are recorded when they occur.

However, the mercantile system has a number of limitations. It does not provide an accurate picture of a company's financial position, as it does not take into account outstanding debts or unpaid invoices. It also does not provide a clear picture of a company's profitability, as it does not take into account the timing of payments.

Despite its limitations, the mercantile system is still widely used, particularly in small businesses and in countries where the accrual basis of accounting is not well-established. It is also sometimes used in conjunction with the accrual basis, with businesses using the mercantile system for tax purposes and the accrual basis for internal reporting.

In conclusion, the mercantile system of accounting is a method of recording financial transactions at the time of sale or purchase, rather than when payment is received or made. While it has some advantages, it also has a number of limitations, and is not as comprehensive as the accrual basis of accounting. However, it is still widely used in small businesses and in certain countries, and is sometimes used in conjunction with the accrual basis.