Short run equilibrium of a firm under perfect competition. Equilibrium under Perfect Competition: Perfectly Competitive Market 2022-10-25

Short run equilibrium of a firm under perfect competition Rating:

7,3/10

569

reviews

In a perfectly competitive market, a firm is a price taker and has no control over the market price of the good or service it produces. The firm must accept the market price as given and can only adjust its quantity of output in response to changes in the market price. In the short run, the firm has some flexibility in terms of its level of production, as it can adjust the quantity of output it produces by changing the use of its variable inputs, such as labor and raw materials.

At any given market price, the firm's profit-maximizing level of output is determined by the intersection of its marginal revenue curve and marginal cost curve. Marginal revenue is the additional revenue a firm receives from selling one additional unit of output, and marginal cost is the additional cost a firm incurs from producing one additional unit of output. The profit-maximizing level of output is where marginal revenue equals marginal cost, as this is the point at which the firm is able to generate the highest level of profit.

If the market price is above the firm's average total cost, then the firm will be able to earn a profit. In this case, the firm has an incentive to increase its level of production in order to take advantage of the positive profit margin. On the other hand, if the market price is below the firm's average total cost, then the firm will incur a loss. In this case, the firm has an incentive to decrease its level of production in order to minimize its losses.

In the short run, a firm operating in a perfectly competitive market will achieve equilibrium at the level of output where marginal revenue equals marginal cost and the market price equals the firm's average total cost. At this point, the firm is earning the maximum profit possible given its fixed level of capital and other fixed inputs.

It is important to note that in the long run, all firms in a perfectly competitive market are able to enter and exit the market freely. This means that if a firm is incurring losses in the short run, it may choose to exit the market in the long run in order to avoid further losses. On the other hand, if a firm is earning profits in the short run, new firms may enter the market in the long run in order to try to capture a share of those profits. This process of entry and exit helps to keep the market supply and demand in balance, and ultimately leads to a long-run equilibrium where firms are earning zero economic profits.

How to Attain Equilibrium of a Firm under Perfect Competition?

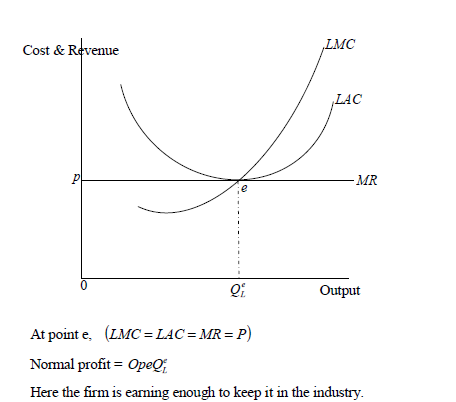

The reason being, in the short period fixed factors like machinery and plants cannot be changed. In case the price is above the long-run AC curve firms will be earning supernormal profits. All curves meet at this point E and the firm produces OQ optimum quantity and sell it at OP price. Therefore, the industry will be in equilibrium, when above given conditions are fulfilled. Since the marginal revenue equals the slope of the total о revenue curve and the marginal cost equals the slope of the tangent to the total cost curve, it follows that where the slopes of the total cost and revenue curves are equal as at P and T, the marginal cost equals the marginal revenue. In Figure 3, the maximum amount of profit is measured by TP at OQ output. Total revenue TR earned by producing output OQ is equal to the area OPEQ, while the total costs are equal to the area ORTQ.

Short Run Equilibrium of a Firm under Perfect Competition

ADVERTISEMENTS: The firm is in equilibrium when it produces the output that maximizes the difference between total receipts and total costs. The total revenue curve is an upward sloping straight line curve starting from O. Profits increase successively with output between Q 1 and Q and are the maximum at OQ level of output. In real-world markets, assumptions such as perfect information cannot be verified and are only approximated in organized double-auction markets where most agents wait and observe the behaviour of prices before deciding to exchange but in the long-period interpretation perfect information is not necessary, the analysis only aims at determining the average around which market prices gravitate, and for gravitation to operate one does not need perfect information. Under perfect competition, an individual firm is a price taker, that is, it has to accept the prevailing price as a given datum.

Equilibrium of Firm and industry under Perfect competition

In part B of the diagram equilibrium of the firm has been shown. S is thus the shut-down point at which the firm is incurring the maximum loss equal to SK per unit of output. However, it will go out of business only if it fails to cover up variable costs from the sale of goods. After point E the cost is decreasing and it is in the interest of the firm to carry on production. The firm is in equilibrium maximizes its profit at the level of output defined by the intersection of the MC and the MR curves point e in figure 5.

Firm C incurs a loss though it attains equilibrium at point E C. What are the main assumptions under the short-run period of a competitive firm? Since revenue OP BE BQ B for OQ B output is the same as that of its cost of production OP BE BQ B , Firm B enjoys only normal profit. It is an upward looking, or positively sloped, curve. Thus, we conclude that industry will be in equilibrium at that level of price end output, where demand curve and supply curve intersect each other. And, it incurs a cost of production to the extent of OCDQ A. Constant Cost Condition : The constant cost conditions mean that the industry is a scale neutral. Each firm would be producing OQ output and earning normal profits at the maximum average total costs QL.

The Equilibrium of the Firm under Perfect Competition

A firm's price will be determined at this point. A firm earns normal profits when the MR curve is tangent to the AC curve at its minimum point. The firm under perfect competition is a price taker and not price-maker. At this price, every firm is making only profit. At this point, equilibrium price is OP 1 and industry supply is OQ 1. Equilibrium of a Competitive Firm in the Long Run : ADVERTISEMENTS: Long run is that time period when firms can adjust their fixed inputs. The firms will continue entering into the industry until the price is equal to average cost so that all firms are earning only normal profits.

Equilibrium of a Competitive Firm in the Short Run and Long Run

All firms have perfect knowledge about price and output. On the other hand, the firm may change, in the long run, the use of all the inputs, variable and fixed, by required amounts to increase its q. Total supernormal profit of a firm is PECD. When the price is OP 1 the output is OQ 1 and equilibrium of the firm is at E 1. We get a long run supply curve e 1e 2 by joining e 1 and e 2, which is a straight line parallel to quantity axis. If the firm decides to operate, the firm will continue to produce where marginal revenue equals marginal costs because these conditions insure not only profit maximization loss minimization but also maximum contribution.

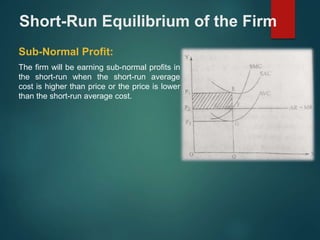

Since perfectly competitive firms sell additional units of output at the same price, marginal revenue curve coincides with average revenue curve. The firm will be in equilibrium at point E 1 or output 0Q 1 since at E 1 marginal cost equals to marginal revenue as well as marginal cost curve cuts marginal revenue curve from below. These comparisons will be made after the firm has made the necessary and feasible long-term adjustments. It produces a quantity depending upon its cost structure. Supernormal Profits: The firm will be earning supernormal profits in the short-run when price is higher than the short-run average cost, as shown in Figure 2 A. The short-run equilibrium of the firm can be explained with the help of the marginal analysis as well as with total cost-revenue analysis.

On the other hand, if the average cost is greater than the average revenue, then the firm is bearing a loss. Price determination will take place at this level only. A firm with a superior entrepreneur than the others will be able to produce the same output at lower costs. Equilibrium under Perfect Competition : As such, equilibrium under perfect competition has to be discussed at two levels: at the level of a firm and at the level of an industry. Situation when a firm decides to continue operating in the short run even when incurring losses. But it makes the equilibrium of the firm a cumbersome and difficult analysis particularly when one has to compare the change in cost and revenue resulting from a change in the volume of output.