Demand and supply are fundamental concepts in economics that describe the relationship between the quantity of a good or service that consumers are willing and able to purchase, and the quantity of that good or service that producers are willing and able to provide. Understanding the forces of demand and supply is crucial for understanding how market economies operate and how prices are determined.

Demand refers to the quantity of a good or service that consumers are willing to purchase at a given price. It is represented on a graph by a downward-sloping curve, indicating that as the price of a good or service increases, the quantity of that good or service that consumers are willing to purchase decreases. This relationship is known as the law of demand.

The law of demand is driven by several factors, including the income of consumers, the prices of related goods or services, and the preferences and tastes of consumers. For example, if the price of a good or service increases, consumers may choose to purchase less of it or switch to a substitute good or service that is cheaper. On the other hand, if the income of consumers increases, they may be willing to purchase more of a good or service, even if its price remains the same.

Supply, on the other hand, refers to the quantity of a good or service that producers are willing and able to provide at a given price. It is represented on a graph by an upward-sloping curve, indicating that as the price of a good or service increases, the quantity of that good or service that producers are willing and able to provide also increases. This relationship is known as the law of supply.

The law of supply is driven by several factors, including the cost of production, the availability of raw materials and other inputs, and the technology and skills of producers. For example, if the cost of production increases, producers may be less willing or able to provide a good or service, leading to a decrease in supply. On the other hand, if the availability of raw materials or other inputs improves, or if technology and skills improve, producers may be more willing and able to provide a good or service, leading to an increase in supply.

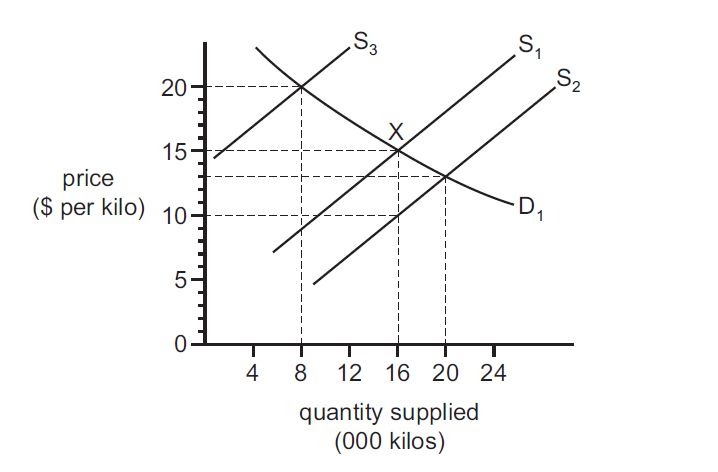

The intersection of the demand and supply curves determines the equilibrium price and quantity of a good or service in a market. At this point, the quantity of a good or service that consumers are willing and able to purchase is equal to the quantity of a good or service that producers are willing and able to provide. Any changes in demand or supply can cause the equilibrium price and quantity to shift.

For example, if the demand for a good or service increases, the demand curve will shift to the right, causing the equilibrium price to increase and the equilibrium quantity to increase as well. On the other hand, if the supply of a good or service increases, the supply curve will shift to the right, causing the equilibrium price to decrease and the equilibrium quantity to increase.

In summary, demand and supply are crucial concepts in economics that describe the relationship between the quantity of a good or service that consumers are willing and able to purchase, and the quantity of that good or service that producers are willing and able to provide. Understanding the forces of demand and supply is essential for understanding how market economies operate and how prices are determined.