The contribution approach to pricing is a strategy that focuses on the costs and revenues associated with a particular product or service, rather than market conditions or competition. This approach aims to determine the price of a product or service by calculating the contribution it makes to the overall profitability of a business.

There are several key elements to the contribution approach to pricing. The first is understanding the costs associated with a product or service, including both direct and indirect costs. Direct costs are those that are directly related to the production of a product or service, such as materials and labor. Indirect costs, on the other hand, are overhead expenses that are not directly tied to a specific product or service, such as rent and utilities.

The second element of the contribution approach to pricing is determining the desired level of profitability for a product or service. This may involve setting a specific target profit margin or simply determining the minimum amount of profit that is necessary to sustain the business.

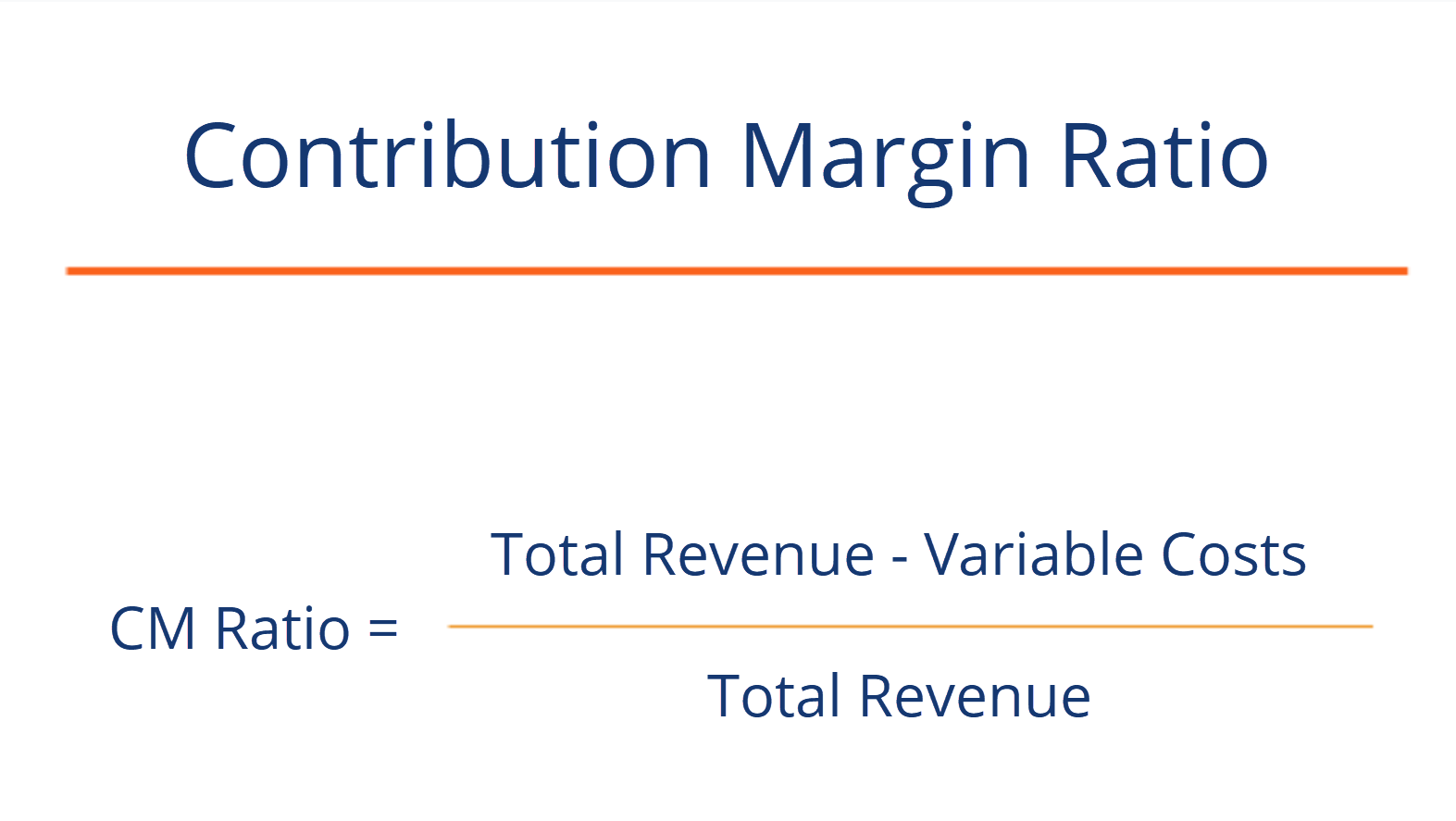

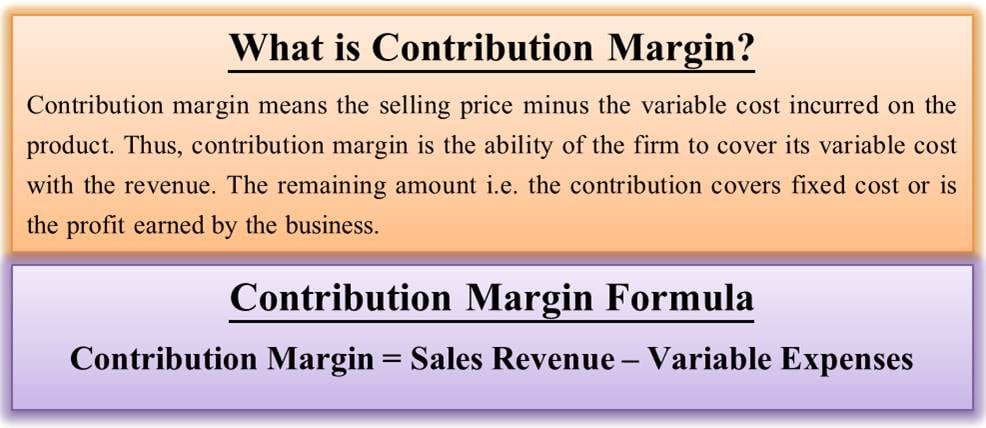

Once the costs and desired profitability of a product or service are understood, the next step is to set the price. This can be done by dividing the desired profit by the contribution margin, which is calculated by subtracting the total costs from the selling price. For example, if the selling price of a product is $100 and the total costs are $70, the contribution margin would be $30. If the desired profit is $20, the price would be set at $90, since this would result in a profit of $20 ($90 - $70).

There are several advantages to the contribution approach to pricing. One of the main benefits is that it allows a business to focus on the costs and revenues associated with a specific product or service, rather than being influenced by external factors such as market conditions or competition. This can help a business to better understand the true value of its products or services and set prices accordingly.

Additionally, the contribution approach to pricing can help a business to better allocate its resources and make informed decisions about which products or services to focus on. By understanding the contribution that each product or service makes to the overall profitability of the business, a company can prioritize those that are most profitable and potentially discontinue or reduce investment in those that are not.

Overall, the contribution approach to pricing is a valuable strategy for businesses that want to focus on the costs and revenues associated with their products or services and make informed decisions about pricing and resource allocation. By understanding the contribution that each product or service makes to the overall profitability of the business, companies can set prices that reflect the true value of their offerings and make more informed decisions about which products or services to focus on.