Au 342 auditing accounting estimates. A refined approach to auditing accounting estimates 2022-10-11

Au 342 auditing accounting estimates Rating:

9,4/10

1260

reviews

Auditing accounting estimates is an important aspect of the auditing process. Accounting estimates are estimates made by management regarding certain aspects of the financial statements, such as the value of inventory or the useful life of an asset. These estimates can have a significant impact on the financial statements, and it is the responsibility of the auditor to evaluate the reasonableness of these estimates.

The auditor's evaluation of accounting estimates is typically performed through a combination of substantive testing and testing of controls. Substantive testing involves the auditor evaluating the underlying assumptions and data used by management to make the estimate. This may involve reviewing supporting documentation, comparing the estimate to industry benchmarks or prior year estimates, or performing other tests to verify the accuracy of the estimate.

Testing of controls involves the auditor evaluating the internal controls in place to ensure that the estimate is being made in a consistent and reliable manner. This may include evaluating the processes used to make the estimate, the training and expertise of the individuals involved in the process, and the documentation supporting the estimate.

The auditor must also consider the risks associated with the estimate and whether additional audit procedures are necessary to address those risks. For example, if the estimate has a significant impact on the financial statements or if there is a high level of uncertainty associated with the estimate, the auditor may need to perform additional procedures to ensure the estimate is reasonable.

In addition to evaluating the reasonableness of the estimate itself, the auditor must also consider the presentation and disclosure of the estimate in the financial statements. This includes evaluating whether the estimate is appropriately classified and whether the required disclosures are made in accordance with accounting standards.

In conclusion, auditing accounting estimates is a crucial part of the auditing process. It requires the auditor to evaluate the reasonableness of the estimate, the controls in place to support the estimate, and the presentation and disclosure of the estimate in the financial statements. Proper auditing of accounting estimates helps to ensure the accuracy and reliability of the financial statements.

AU 342.10

It was amended, effective for audits of fiscal years beginning on or after December 15, 2010. If the unaudited voluntary disclosures are located on the face of the financial statements or in the footnotes, the voluntary disclosures should be labeled "unaudited. Furthermore, amounts ultimately realized by ABC Company from the disposal of assets may vary significantly from the fair values presented. See section 9342 for interpretations of this section. In our opinion, the supplemental fair value balance sheet referred to above presents fairly, in all material respects, the information set forth therein as described in Note X. See Review subsequent events or transactions.

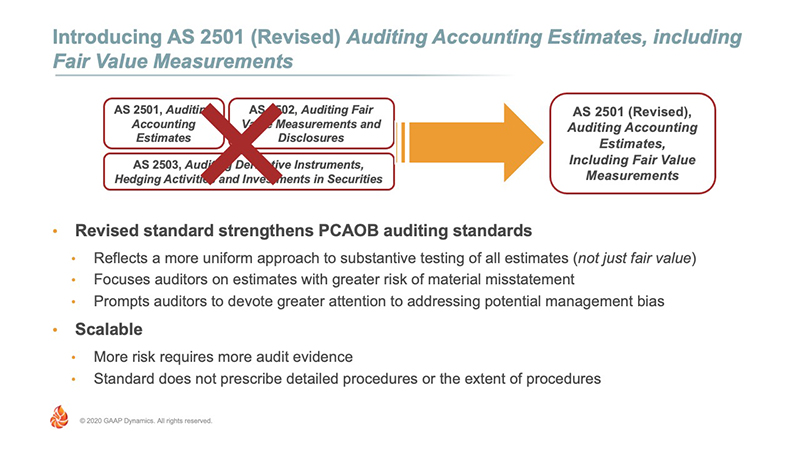

See This section provides guidance to auditors on obtaining and evaluating sufficient appropriate evidential matter to support significant accounting estimates in an audit of financial statements in accordance with generally accepted auditing standards. Accordingly, when planning and performing procedures to evaluate accounting estimates, the auditor should consider, with an attitude of professional skepticism, both the subjective and objective factors. Auditing Accounting Estimates 2057 AU Section 342 Auditing Accounting Estimates Source: SAS No. Accounting estimates are often included in historical financial statements because— a. Note: When performing an integrated audit of financial statements and internal control over financial reporting, the auditor may use any of the three approaches.

Audit Exam 2: Auditing Estimates and Fair Value Flashcards

Consideration of the need to use the work of specialists ´. The list is presented for information only. Based on the auditor's understanding of the facts and circumstances, he may independently develop an expectation as to the estimate by using other key factors or alternative assumptions about those factors. Relevant data concerning events that have already occurred cannot be accumulated on a timely, cost-effective basis. The current versionof the auditing interpretationscan be found Auditing Accounting Estimates: Auditing Interpretations of Section 342 1. Events or transactions sometimes occur subsequent to the date of the balance sheet, but prior to the date of the auditor's report, that are important in identifying and evaluating the reasonableness of accounting estimates or key factors or assumptions used in the preparation of the estimate.

AU-C EFFECTIVE DATE AND SUMMARY OF CHANGES SAS No. Those accounting estimates are reasonable in the circumstances. It should not be considered all-inclusive. What are the risks that would cause it to be materially misstated? Some entities may disclose the information required by FASB Statement No. In such circumstances, an evaluation of the estimate or of a key factor or assumption may be minimized or unnecessary as the event or transaction can be used by the auditor in evaluating their reasonableness.

Accounting estimates in historical financial statements measure the effects of past business transactions or events, or the present status of an asset or liability. Estimates are based on subjective as well as objective factors and, as a result, judgment is required to estimate an amount at the date of the financial statements. As estimates are based on subjective as well as objec- tive factors, it may be difficult for management to establish controls over them. For purposes of this section, an accounting estimate is an approximation of a financial statement element, item, or account. Estimates are based on subjective as well as objective factors and, as a result, judgment is required to estimate an amount at the date of the financial statements. The first issue is determining whether the assumptions underlying those estimates are reasonable. However, the work that the auditor performs as part of the audit of internal control over financial reporting should necessarily inform the auditor's decisions about the approach he or she takes to auditing an estimate because, as part of the audit of internal control over financial reporting, the auditor would be required to obtain an understanding of the process management used to develop the estimate and to test controls over all relevant assertions related to the estimate.

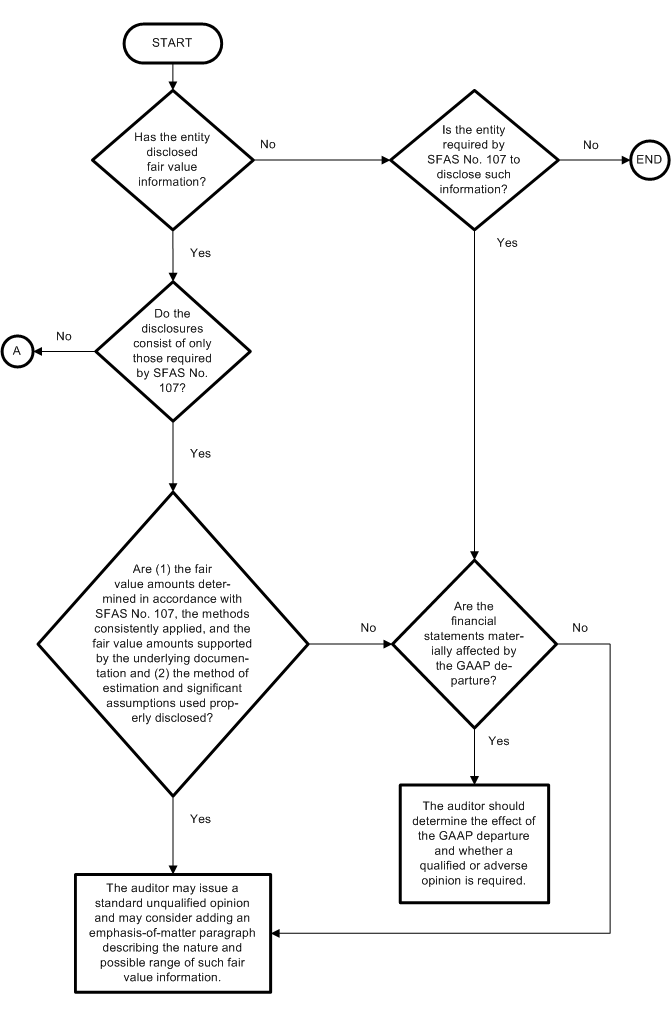

Events or transactions sometimes occur subsequent to the date of the balance sheet, but prior to the completion of fieldwork, that are important in identifying and evaluating the reasonableness of accounting estimates or key factors or assumptions used in the preparation of the estimate. The auditor should also consider whether the difference between estimates best supported by the audit evidence and the estimates included in the financial statements, which are individually reasonable, indicate a possible bias on the part of the entity's management. The auditor may add an emphasis-of-matter paragraph describing the nature and possible range of such fair value information especially when management's best estimate of value is used in the absence of quoted market values FASB Statement No. For purposes of this section, an accounting estimate is an approximation of a financial statement element, item, or account. See When the audited disclosures do not constitute a complete balance sheet presentation and are located on the face of the financial statements or in the footnotes, the auditor may issue a standard unqualified opinion and need not mention the disclosures in the report.

In such circumstances, an evaluation of the estimate or of a key factor or assumption may be minimized or unnecessary as the event or transaction can be used by the auditor in evaluating their reasonableness. Even when management's estimation process involves competent personnel using relevant and reliable data, there is potential for bias in the subjective factors. See Paragraphs 24 through 27 of Auditing Standard No. Examples of accounting estimates include net realizable values of inventory and accounts receivable, property and casualty insurance loss reserves, revenues from contracts accounted for by the percentage-of-completion method, and pension and warranty expenses. Even when management's estimation process involves competent personnel using relevant and reliable data, there is potential for bias in the subjective factors. The PCAOB and IAASB standards emphasize the need for professional skepticism.

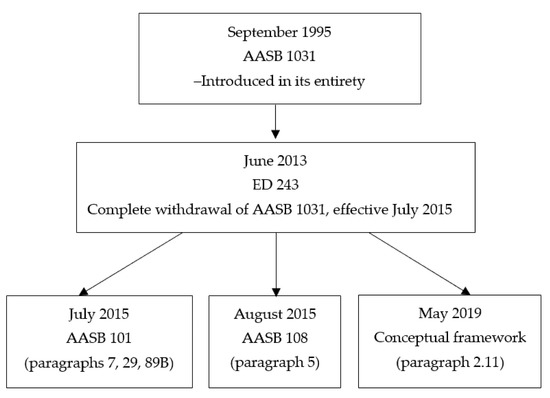

. Early application of the provisions of this section is permissible. . AU-C 540 supersedes AU-C 328, Auditing Fair Value Measurements and Disclosures, and AU 342, Auditing Accounting Estimates. Does this person have a good reputation, and are they objective? As described in Note X, the supplemental fair value balance sheet has been prepared by management to present relevant financial information that is not provided by the historical-cost balance sheets and is not intended to be a presentation in conformity with generally accepted accounting principles. Harding noted that even the language auditors use can introduce unconscious bias.

AU-C 540 does not change the extant requirements of AU 342 in any significant respect. Receivables: Revenues: Uncollectible receivables Airline passenger revenue Allowance for loan losses Subscription income Uncollectible pledges Freight and cargo revenue Dues income Inventories: Losses on sales contracts Obsolete inventory Net realizable value of inventories where future selling prices and future costs are involved Contracts: Losses on purchase commitments Revenue to be earned Costs to be incurred Financial instruments: Percent of completion Valuation of securities Trading versus investment security classification Leases: Probability of high correlation of a hedge Initial direct costs Sales of securities with puts and calls Executory costs Residual values Productive facilities, natural resources and intangibles: Useful lives and residual values Litigation: Depreciation and amortization methods Probability of loss Recoverability of costs Amount of loss Recoverable reserves Rates: Accruals: Annual effective tax rate in interim reporting Property and casualty insurance company loss reserves Imputed interest rates on receivables and payables Compensation in stock option plans and deferred plans Gross profit rates under program method of accounting Warranty claims Taxes on real and personal property Other: Renegotiation refunds Losses and net realizable value on disposal of segment or restructuring of a business Actuarial assumptions in pension costs Fair values in nonmonetary exchanges Interim period costs in interim reporting Current values in personal financial statements Footnotes AU Section 342 — Auditing Accounting Estimates : fn1 Additional examples of accounting estimates included in historical financial statements are presented in paragraph. For example, if a client has a defined benefit pension obligation, and the information given to the actuary is incorrect, then the estimate is going to be incorrect. If the entity has not disclosed required fair value information, the auditor should evaluate whether the financial statements are materially affected by the departure from generally accepted accounting principles. The following auditing standard is not the current version and does not reflect any amendments effective on or after December 31, 2016. Management's judgment is normally based on its knowledge and experience about past and current events and its assumptions about conditions it expects to exist and courses of action it expects to take. Warranty claims Uncollectible accounts Pension obligations - several estimates Self-insured amounts e.

For audits of ±scal years beginning before December 15, 2010, click here. Accounting estimates are included in historical financial statements because 1 the measurement of some amounts or the valuation of some accounts is uncertain, pending the outcome of future events, or 2 relevant data concerning events that have already occurred cannot be accumulated on a timely cost-effective basis. The measurement of some amounts or the valuation of some accounts is uncertain, pending the outcome of future events. Management's judgment is normally based on its knowledge and experience about past and current events and its assumptions about conditions it expects to exist and courses of action it expects to take. In addition, the supplemental fair value balance sheet does not purport to present the net realizable, liquidation, or market value of ABC Company as a whole. AU DEFINITIONS OF TERMS Accounting estimate.