If I were a teacher, I would be filled with excitement and enthusiasm for the opportunity to shape the minds of young learners. I would approach each day with energy and dedication, striving to create a classroom environment that is both engaging and supportive.

As a teacher, my primary goal would be to inspire a love of learning in my students. I would strive to create a curriculum that is challenging and rewarding, and that allows students to explore their interests and passions. I would also work to foster a sense of community in my classroom, encouraging students to support and learn from one another.

In order to be an effective teacher, I would also need to be patient, understanding, and open-minded. I would listen to my students' concerns and questions, and do my best to help them find the answers they need. I would also be willing to adapt my teaching style to meet the needs of individual students, whether that means providing extra support for struggling learners or offering more advanced material for those who are ready for a greater challenge.

In addition to being a teacher, I would also strive to be a role model for my students. I would set high standards for myself and work to live up to them, always striving to be the best version of myself. I would also encourage my students to set their own high standards and to work towards achieving their goals.

Overall, if I were a teacher, I would be deeply committed to helping my students grow and succeed. I would work hard to create a positive and supportive learning environment, and to inspire a love of learning in all of my students.

AF210 FINAL Exam

The amounts of translated cash flows will not vary with the choice of functional currency, because historical exchange rates are used to translate all cash flows. However, other transactions and account balances denominated in the old functional currency, which were not previously translated, now do need to be translated, and therefore are affected by exchange rate movements. An economic entity may span more than one legal entity, but is not a legal entity in itself. It is made each time the consolidation is performed in order to adjust the carrying value of the controlled entity's non-current assets to their fair value. Section A: 30 Marks This section contains 15 Multiple Choice questions worth 2 marks each.

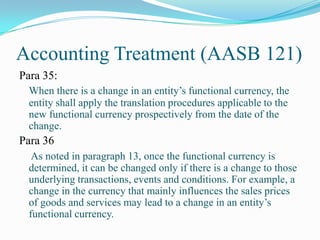

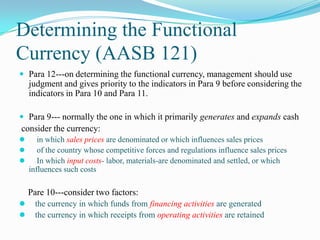

According to AASB 121 functional currency is the currency of the primary

Year-end date is 30 June. If the functional local currency of the foreign operation differs from the presentation currency, an appreciation of the functional currency, where the net assets of the foreign operation are positive, can result in a foreign exchange translation gain, but adverse economic consequences for investors in the foreign operation in the form of reduced profits, and reduced value of their investment. You are to spend about 45 minutes on this section. The concept of an economic entity emphasises substance over legal form. Similarly, translated foreign exchange gains and losses included in the other comprehensive income of the subsidiary will be included in the consolidated other comprehensive income, subject to consolidation eliminations and adjustments.

Furthermore, the amount of the translation gain or loss arising upon translating the functional currency financial statements of the subsidiary into the presentation currency of the group, included in consolidated other comprehensive income will also differ. Cash flows of the group, which are denominated in a currency other than the presentation currency of the group, are translated into the presentation currency using the historical exchange rates at the date the cash flow occurs AASB 121. The foreign operation may need to reduce its selling prices to remain competitive, which would result in lower profits or increased losses , and reduce the value of the foreign operation. Therefore, an appreciation of the local functional currency can result in a foreign currency translation gain, but adverse economic consequences for investors in the foreign operation. Question 17: Statement of cash flow 20 Marks Selected financial statements of The Big Figure Ltd are shown below.

AASB 121 specifies that post acquisition movements in equity other than retained

An economic entity is one that combines one or more legal entities with synergy such that they each make higher returns than they would individually. All existing rights in this material are reserved outside Australia. Therefore, choosing a different functional currency will affect the reported profits of the subsidiary. Subsequent to the reporting date, the court handed down its decision and upheld a substantial claim for damages. Warning: TT: undefined function: 32 University of the South Pacific School of Accounting and Finance Semester 1, 2019 AF210 Financial Accounting Face to Face and Blended mode Final Exam Instructions There are 11 pages in this exam paper, including this cover page There are two sections in this exam paper, Section A and Section B. The contingent liability note should remain as it is because it reflects the situation existing at reporting date.

CS代考 AASB 121.08 as “the currency of the primary economic environment in which t

Required: a Provide the relevant journal entries of Oriental Building solutions for the year ending 30 June 2020. As paragraph 22 of AASB 121 states: For practical reasons, a rate that approximates the actual rate at the date of the transaction is often used, for example, an average rate for a week or a month might be used for all transactions in each foreign currency occurring during that period. The amount is payable on 1 August 2020. The above requirements relate to accounts contained within the statement of comprehensive income. If an entity ceases to effectively produce increased returns in this way it becomes uneconomic. The settlement is for a material amount.

as defined in AASB 121 AASB 13987 A hedge of the foreign currency risk of a firm

Foreign exchange gains and losses resulting from translating foreign currency non-monetary items, which were restated to fair value into the functional currency, are included in the other comprehensive income of the subsidiary AASB 121. The currency that influences the operating costs of CI Ltd is the Cayman dollar KYD , as CI Ltd pays operating costs such as accounting and taxation in KYD. Reproduction outside Australia in unaltered form retaining this notice is permitted for personal and non-commercial use only. In relation to accounts that would generally be presented within the statement of financial position, paragraph 23 of AASB 121 states: At the end of each reporting period: a foreign currency monetary items shall be translated using the closing rate b non-monetary items that are measured in terms of historical cost in a foreign currency shall be translated using the exchange rate at the date of the transaction, and c non-monetary items that are measured at fair value in a foreign currency shall be translated using the exchange rates at the date when the fair value was determined 288 Translating the accounts into a particular functional currency cont. This foreign exchange gain will be adjusted for the effect of changes in net assets including changes attributable to total comprehensive income for the period and dividends. The relevant exchange rate for a group where the presentation currency is, say, AUD is the exchange rate for exchanging AUD with the currency in which the cash flow is denominated, regardless of the functional currency of the subsidiary. The opening net assets translated at the closing exchange rate at the end of the period is a greater amount expressed in terms of the presentation currency of the entity than the opening net assets translated using the opening exchange rate at the beginning of the period.

Shalom Ltd uses fair-value hedge accounting. No reporting is required. It requires the delivery of the US dollars on 1 August 2020. How should this transaction be recorded in the financial statements according to IFRS? Therefore, the translated foreign exchange gains and losses included in the reported profit of the subsidiary will also be included in the consolidated profit. It is made each time the consolidation is performed in order to eliminate the parent entity's investment in the controlled entity against the equity of the controlled entity.

The accident occurred after reporting date, but Cavalier has settled quickly so the outcome is now known before the authorisation date of the financial statements. Additional information that would be relevant to determining the functional currency of CI Ltd includes: 1 The currency in which CI Ltd obtains funds from financing activities AASB 121. It is made once at the time of the first consolidation of the economic entity's accounts in order to eliminate the parent entity's investment in the subsidiary against the non-monetary assets of the controlled entity. According to IFRS how should this event be treated in the financial statements? You have 10 minutes to read the paper and 3 hours to write your answers. . Therefore, the translated amount of these foreign exchange gains and losses included in consolidated profit and consolidated other comprehensive income subject to consolidation eliminations and adjustments will also differ.