Costs are an important concept in economics because they play a crucial role in decision-making and resource allocation. In a market economy, costs help firms decide how to produce goods and services, what prices to charge for them, and whether to enter or exit a particular market. Costs also influence consumer behavior, as they help individuals decide what to buy and how much to buy.

There are several types of costs that are important in economics. The most basic type is opportunity cost, which is the value of the next best alternative that is given up when a decision is made. For example, if an individual decides to go to college, the opportunity cost is the wages they could have earned if they had not gone to college.

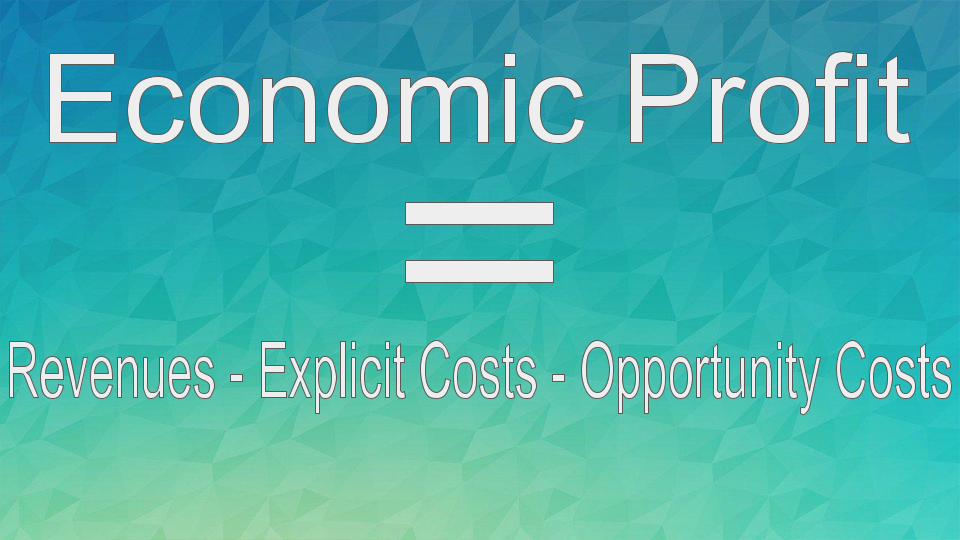

There are also explicit costs, which are costs that involve an outlay of money, such as the cost of materials, labor, and rent. Implicit costs, on the other hand, are costs that do not involve an outlay of money, such as the opportunity cost of using one's own capital or the value of one's own time.

Total cost is the sum of explicit and implicit costs, and it is an important concept for firms because it helps them determine the minimum price they need to charge in order to break even. Average total cost is the total cost divided by the quantity of goods produced, and it helps firms determine the minimum price they need to charge in order to make a profit.

Costs are also important in economics because they help to allocate resources efficiently. In a market economy, firms and consumers make decisions based on the costs and benefits of their actions. When the costs of producing a good or service are high, firms are less likely to produce it, and consumers are less likely to buy it. On the other hand, when the costs of producing a good or service are low, firms are more likely to produce it, and consumers are more likely to buy it. This process helps to ensure that resources are used efficiently and that goods and services are produced where they are most valued.

In conclusion, costs are an important concept in economics because they play a crucial role in decision-making and resource allocation. Understanding costs is essential for firms to make production and pricing decisions, and for consumers to make consumption decisions. Costs also help to allocate resources efficiently in a market economy.

Importance of economics in our daily lives

How does opportunity relate to cost principles? The real value of our savings will decline — unless we can secure an interest rate higher than the rate of inflation. Yes, that's a benefit. While economists are often concerned with the past, they are more often concerned with the future. Why does this matter? Because by definition they are unseen, opportunity costs can be easily overlooked if one is not careful. Why is opportunity cost important to economic agents? If the cost is too high, the product's price might be too high and will not be bought by consumers. When you hear classmates, co-workers, or political candidates talking about economics, you will be able to distinguish between common sense and nonsense.

(a) Why is choice important in economics? (b) What are the costs of choice?

To an economist, "value" is the same as marginal cost. Keep in mind that economic costs are different than accounting costs; accounting costs refers strictly to monetary value, while economic cost includes monetary value as well as other values, like resources and satisfaction. The study of economics helps people understand the world around them. Gross profit continues to grow at 30. Why opportunity cost is relevant in decision-making? You need to be able to vote intelligently on budgets, regulations, and laws in general. In other words, each time resources are allocated, there is a cost of using them for one purpose over another. At the ice cream parlor, you have to choose between rocky road and strawberry.

What is opportunity cost and why is it important in economics?

Those were also benefits. Economics can generally be broken down into macroeconomics, which concentrates on the behavior of the economy as a whole, and microeconomics, which focuses on individual people and businesses. Nothing you do at that point will get your "money's worth. Although opportunity costs are an economic concept, they play a part in every personal decision that we make. By understanding the true financial cost of each outcome, anyone can make more logical and beneficial decisions. What is a real life example of opportunity cost? Of course, this assumes he does not paint his house for fun! How can a group of workers, each specializing in certain tasks, produce so much more than the same number of workers who try to produce the entire good or service by themselves? Because our actions are intended to create value, and we always aim to maximize that subjectively understood value.