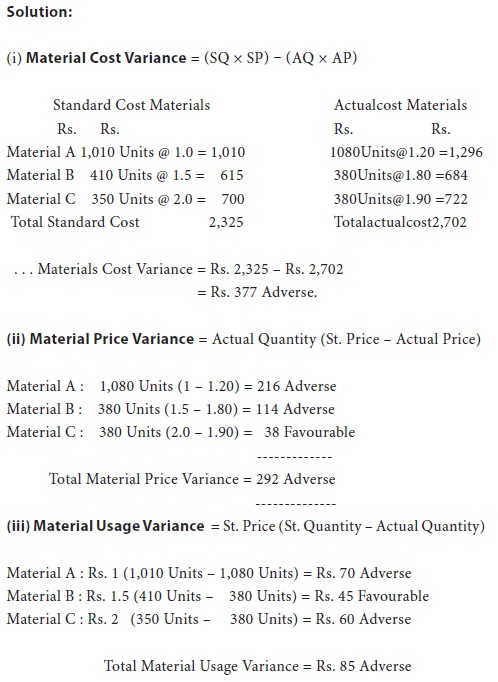

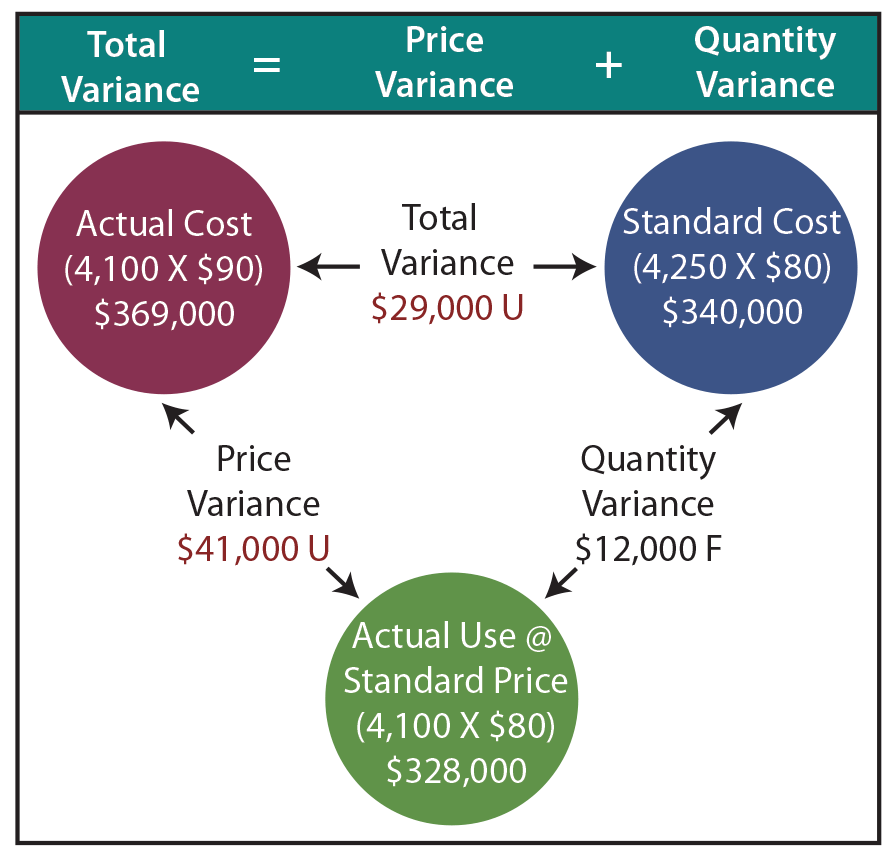

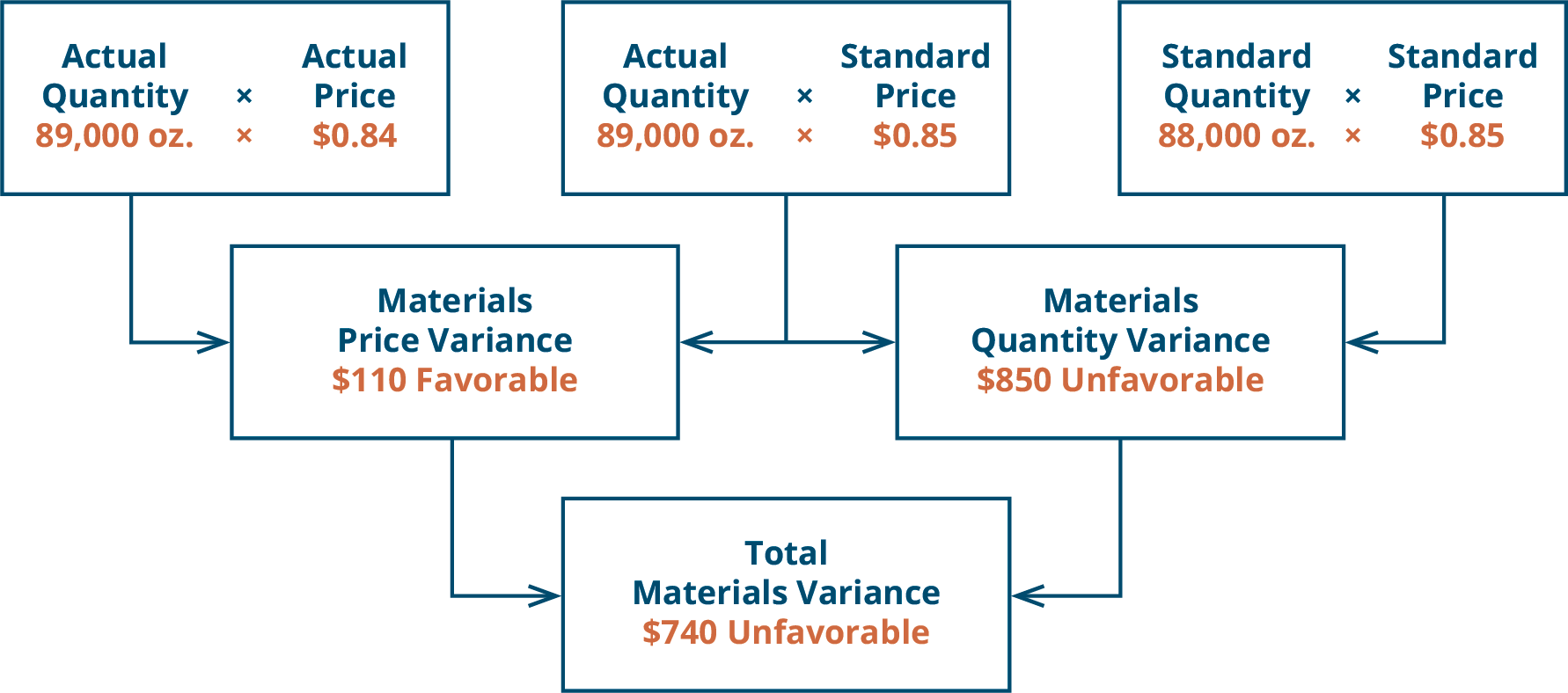

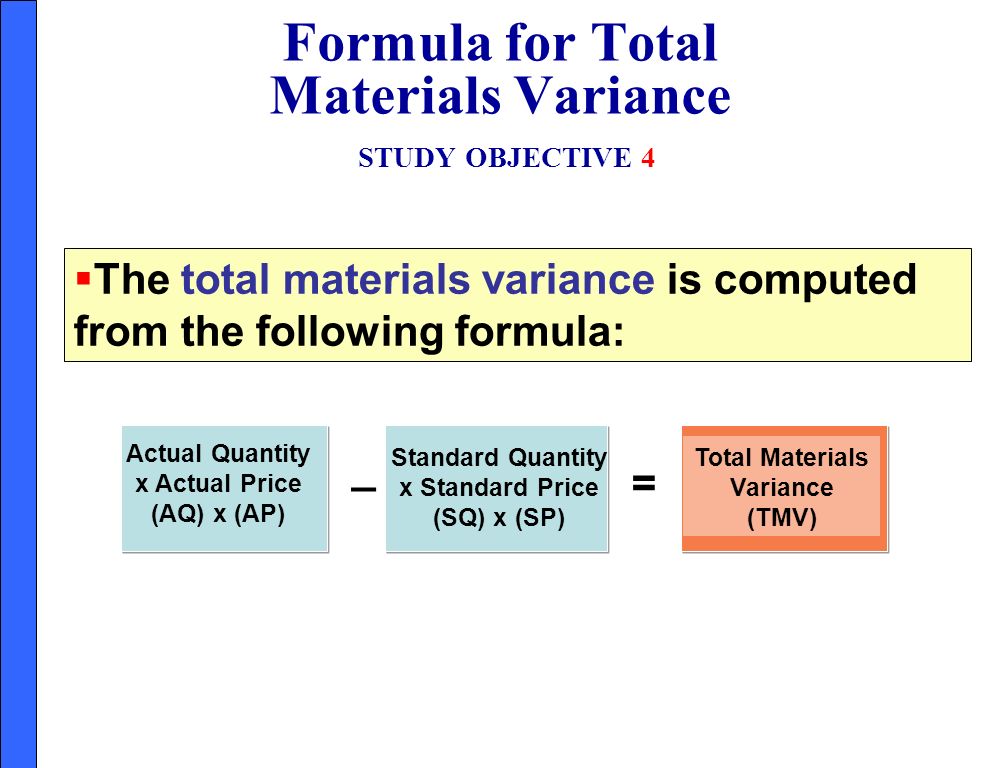

Total materials variance (TMV) is a measure of the difference between the actual cost of materials used in a production process and the budgeted cost of those materials. It is a tool used in variance analysis, which is the process of comparing actual results to planned or budgeted amounts in order to identify deviations and understand the reasons for those deviations.

TMV is calculated by subtracting the budgeted cost of materials from the actual cost of materials and expressing the result as a percentage of the budgeted cost. For example, if the budgeted cost of materials for a production process is $10,000 and the actual cost is $12,000, the TMV would be $2,000 or 20% of the budgeted cost.

There are several factors that can cause TMV to occur, including changes in the price of materials, changes in the quantity of materials used, and changes in the efficiency of the production process. For example, if the price of a raw material increases, the cost of materials will also increase, resulting in a positive TMV. On the other hand, if the production process becomes more efficient and requires fewer materials, the cost of materials will decrease, resulting in a negative TMV.

TMV is an important metric for managers to monitor because it can have a significant impact on the overall cost of production. If TMV is consistently positive, it may indicate that the production process is not as efficient as it could be and that steps should be taken to reduce the amount of materials used or to find ways to lower the cost of materials. On the other hand, if TMV is consistently negative, it may indicate that the budgeted cost of materials was set too high and that cost savings could be realized by revising the budget.

In conclusion, total materials variance is a measure of the difference between the actual and budgeted cost of materials used in a production process. It is an important metric for managers to monitor in order to understand the reasons for deviations from budget and to identify opportunities for cost savings. By understanding and managing TMV, managers can help to ensure that the production process is as efficient and cost-effective as possible.

Total materials webapi.bu.edu

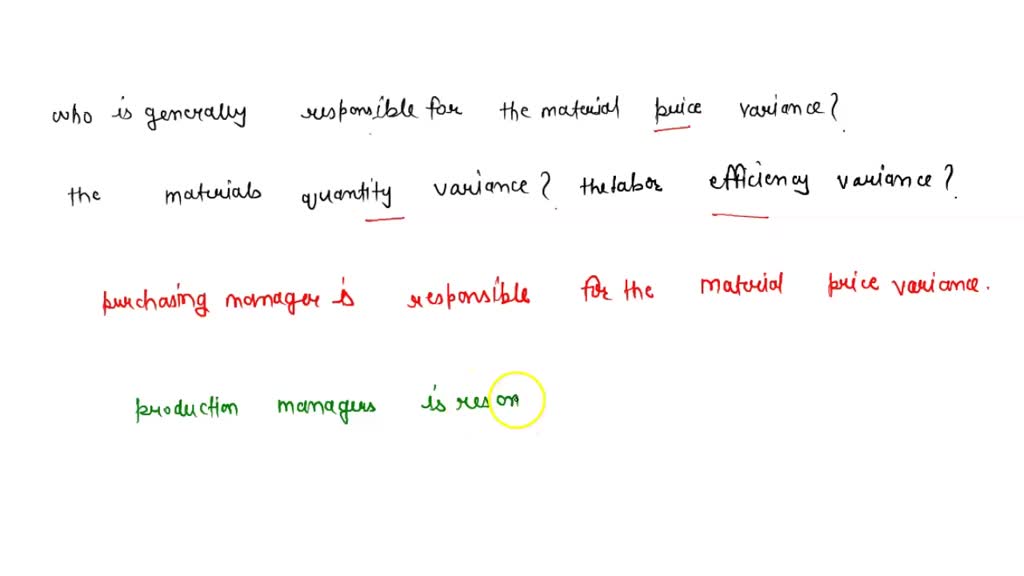

One big difference between the MYV and other variance is that the calculation of other variance is on the basis of input, while MYV depends on the output. These reasons could be emergency purchases, purchase of excessive or deficit quantity, price rise, new taxes, etc. The speakers are sold in bulk to mobile manufacturing companies where complete mobiles are produced. Terms Similar to Material Quantity Variance The material quantity variance is also known as the material usage variance and the material yield variance. And make it a reference and drive and monitor to see that actuals remain as near as possible to the standard estimates. It is useful for determining the ability of a business to incur materials costs close to the levels at which it had planned to incur them. In a year, Company A uses 315,000 kg of plastic to create 35,000 desks or 9 kg to produce one desk.

Material Variance

So, the more scrap, the more the possibility and volume of variance. To make a batch of carrot cakes, you expect to use 60 pounds of carrots. The companies use this optimum mix of materials as the standard to set their cost and budgetary estimations. It is crucial that whenever you calculate any variance, you denote it as favorable or adverse. Please refer to our Customer Relationship Statement and Form ADV Wrap program disclosure available at the SEC's investment adviser public information website: CARBON COLLECTIVE INVESTING, LLC - Investment Adviser Firm sec.

Material quantity variance definition — AccountingTools

Hence, this variance is of quite importance. You expect about 5% of the peaches you order from a local farm to go bad between purchasing and baking day. And it is unfavorable if the estimated cost is lower than the actual cost. You have an unfavorable materials quantity variance when you use more material than expected. There can be many reasons for material usage variance, including the use of sub-standard or defective products, pilferage, wastage, differences in material quality, etc. Scraps also increase in case of a change in acceptable tolerance levels or any change in the inspection process. Your pastry chef told you he accidentally dropped a bowl with 15 pounds of carrots.

Material Price Variance Calculator

Material variances include two factors: 1. Your standard material quantity is 60 pounds. But there could be the other side of the coin too. Prepare a In the carrot cake example, we used more carrots than expected. In cases where the actual price is more than the standard price, the result is A , which means adverse. Conversely, a parsimonious standard allows little room for error, so there is more likely to be a considerable number of unfavorable variances over time.

Material Variances

Material Yield Variance is the variance or the difference between the standard quantity of material consumption estimated and the actual amount of material consumed in production. For example, if suppliers of raw materials are unable to meet the demand, the company may have to look for another supplier. To do this, we need to calculate the MYV using the direct formula, and the answer from both approaches should be the same. The measurement is employed to determine the efficiency of a production process in converting raw materials into finished goods. Overview: What is a materials quantity variance? Cautions In order to avoid unfavorable variances, management has to keep certain things in mind.

[Solved] Total materials variance $ ...

Material Quality If the quality of material degrades, or the company starts procuring low quality, it would also increase the unfavorable variance. Low-quality raw materials, broken machinery, and inadequately trained workers may be to blame for abnormal spoilage. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Abnormal spoilage increases the amount of raw material consumed in manufacturing, creating an unfavorable materials quantity variance. For more details, see our Form CRS, Form ADV Part 2 and other disclosures. A materials quantity variance compares the actual and expected direct material used in manufacturing a product.