Target and life cycle costing. Target and Life Cycle webapi.bu.edu 2022-10-26

Target and life cycle costing Rating:

5,2/10

1792

reviews

Target costing and life cycle costing are two important tools that businesses use to manage their costs and improve their competitiveness.

Target costing involves setting a target cost for a product or service before it is developed. This cost is based on the price that the market is willing to pay, as well as the profit margin that the company hopes to achieve. The target cost is then used as a benchmark throughout the development process to ensure that the final product is produced at a cost that is in line with the target.

One of the main benefits of target costing is that it helps businesses to focus on cost reduction from the very beginning of the product development process. By setting a target cost early on, companies can identify potential cost savings opportunities and take action to eliminate waste and reduce costs. This can help businesses to stay competitive in their markets by offering high-quality products at competitive prices.

Life cycle costing, on the other hand, looks at the costs associated with a product or service over its entire life cycle. This includes the costs of research and development, production, marketing, distribution, and disposal. By considering the costs of a product or service over its entire life cycle, businesses can make more informed decisions about how to allocate their resources and optimize their costs.

For example, a company might choose to invest in more expensive, high-quality materials in the production stage in order to reduce maintenance and repair costs over the life of the product. Or, a company might decide to invest in more efficient manufacturing processes in order to reduce energy and raw material costs over the life of the product.

Both target costing and life cycle costing can help businesses to better manage their costs and improve their competitiveness. By setting clear cost targets and considering the costs of a product or service over its entire life cycle, businesses can make more informed decisions about how to allocate their resources and optimize their costs. This can lead to improved profitability and a stronger bottom line.

Target Costing

You are free to use this image on your website, templates, etc. The look, feel and ease of use, have become key value drivers for the customer. MiMobie Ltd's production of phones and accessories, the manufacturing department tends to reduce the cycles to cut the targeted cost. Value engineering can be broken into stages. Target costing is said to have been developed by Toyota in the 1960s.

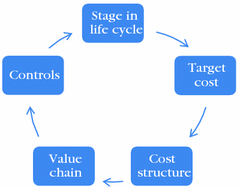

It represents the amount of value the owner will obtain or expect to get eventually when the asset is disposed. Thus, the customer feels more value is delivered. This should include all costs associated with the product. The life cycle costs include all costs incurred from the initial concept emerging from the research and development process to the recycling of materials at the end of the products useful life. An understanding of the stages a product goes through enables you to price accordingly to either manipulate demand low price, demand will rise and the intro stage is shortened or to maximise profit. A few authors have suggested that it should also take account of financing costs. The design cost helps to assess the importance and competitive advantage of the product.

Therefore, if the whole of the life cycle is to be considered it requires a forecast to be made of the pattern of future demand, and the likely response of competitors. It is only natural that a marketing team becomes heavily involved in this process, as much of what is done here is based on customer feedback. In practice the profit expected is after deducting all costs incurred up to the point when the product is ready for sale. The management accounting concept of life cycle costing suggests that considering the costs of the complete product life cycle from cradle to grave, or cradle to cradle, if we consider the recycling after use, can provide additional benefits to the organisation, particularly in the activities of new product development, affordability studies, source selection, and repair or replace decisions. What are the estimated life-cycle revenues? We could extend this definition to explicitly include the cost of recycling materials from the product following the end of its useful life.

Target And Life Cycle webapi.bu.edu [1d479o89w2l2]

The goal is to identify improvements and associated reductions in cost that may allow the company to add previously rejected options. This is commonly referred to as the cradle to grave, or at times referred to as the womb to tomb Drury, 2007 p 541. The point here is that these costs are typically recorded and reported during the manufacturing phase, and therefore unless considered beforehand can create surprises for management. To lower the costs of new products so that the required profit level can be ensured. The benefits of the LLC system are the promotion of the best decision-making criterion for accurate and realistic market assessment in different stages. Its primary purpose is to help management decide whether or not to go ahead with a project or acquire an asset.

Target costs will enable Letscommunication to attain proactive approach to management of costs, orientation to consumers, breaking barriers between departments, empowerment of employees, awareness of employees, enable suppliers partnerships, reduce activities related to non value added activities, foster activities related to lowest cost value and save time on the market. Determine required profit Each product or service that an organisation sells makes a contribution to the overall profit achieved. Typically, conventional costing attempts to work out the cost of producing an item incorporating the costs of resources that are currently used or consumed. Collected data are compared with budgeted costs to check whether expected savings have been realised. The expenditures in the production stages in the mobile phones will identify which will enable the public authorities make predictions on the budgets. A challenge of working with suppliers and outsourcing elements of the production process is determining the exact specification and expectations of performance from the suppliers.

It is through the product life cycle whereby the MiMobie Ltd management would trace costs and revenues of every stage in production over a long period. Target cost of the mobile phones equal to anticipated selling price-desired profit Banerjee, 2006 p 886. Management usually analyses the cost of ownership and operating cost and then eventually chooses the asset with the minimum overall cost. Thus design and production teams must work together to ensure costs are minimised b Minimise the time to market This is the time from the conception of the product to its launch. Techniques such as functional cost analysis and value engineering enable a better understanding and consideration of the trade-off between product function and cost Iranmanesh and Thomson 2008. Hiromoto 1991 suggests that the market based approach to pricing is highly relevant in a competitive market, and that management accountants are able to help to motivate a market-driven behaviour by working as part of the team to derive a market allowable cost, and to ensure continued profitability of the organisation. The members of the team should work together to fully understand the interplay and trade-offs between costs and functionality, and consequently, whilst a broad background is desirable, there may be some training involved in order to make the team operate effectively.

Letscommunication will enhance product profitability. This paper will elaborate on the targeting costing system and life cycle costing system and their competitive advantages to ensure MiMobie Ltd achieves profitability in a volatile and competitive market. Target costing uses a market based approach to pricing to derive an allowable cost for new products, as opposed to deriving the selling price by adding a mark-up on cost. This provides information about the importance of various functionality, and hence identifies sensitive areas where the balance between functionality and cost needs to be carefully managed. It may be that the early price at which the product is introduced may be slightly higher. The increasing awareness of sustainability issues has emphasised the need for organisations to work together through the development of new materials, packaging designs, and recycling systems, as well as new products.

Get Help With Your Essay If you need assistance with writing your essay, our professional essay writing service is here to help! The achievement of MiMobie Ltd has based market competitiveness in prices and product innovation. MiMobie Ltd management has the mandate of ensuring the phones and accessories production meets the quality, deliveries are made on time, and the prices in the market are achieved. The product concept phase involves a zero look. Young, Management Accounting Upper Saddle River, New Jersey: Prentice-Hall, 1997 ; and J. Life cycles costs will enable Letscommunication to manage operating costs effectively. Sundem, Introduction to Management Accounting, 9th edition Englewood Cliffs, New Jersey: Prentice-Hall, 1993. This team approach needs to feed into a process of organisational learning so that future projects benefit from the experience gained, and lessons learned from previous successes and failures.

.jpg)