International convergence of accounting standards refers to the process of bringing accounting standards and practices in different countries closer together, with the goal of creating a common set of standards that can be used globally. This process is important because it helps to improve the comparability and transparency of financial information, which is essential for investors, creditors, and other stakeholders who rely on this information to make informed decisions.

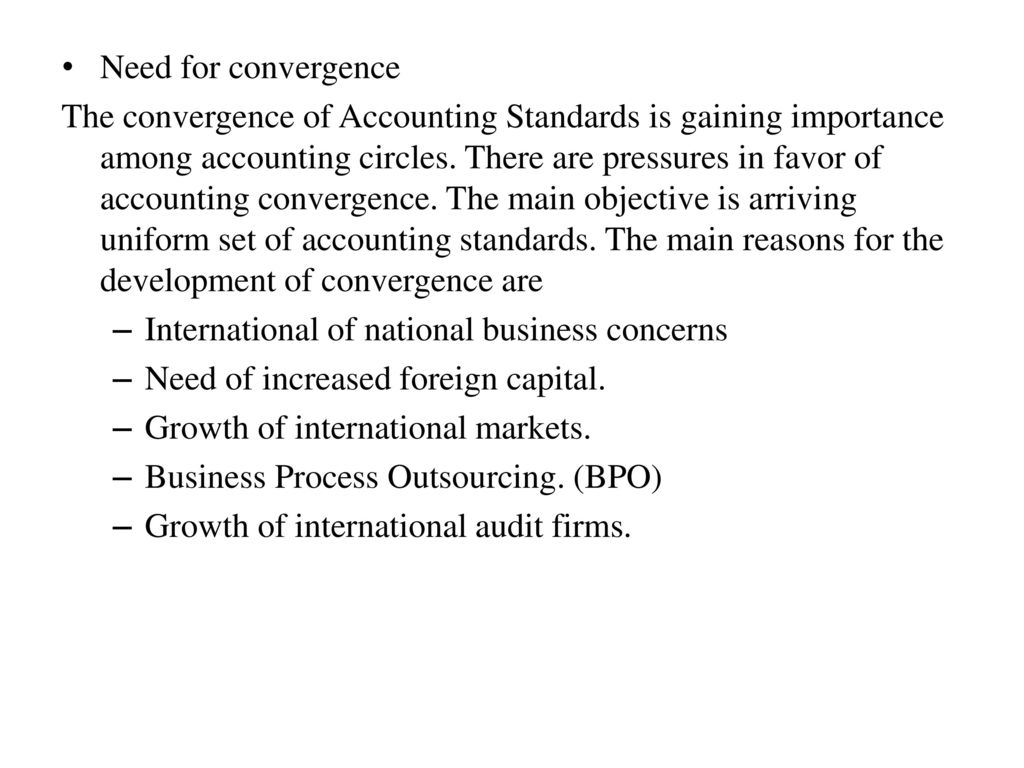

One of the main drivers of international convergence of accounting standards is the increasing globalization of financial markets. As businesses and investors become more interconnected, it becomes increasingly important for financial information to be comparable across borders. This allows investors to easily compare the financial performance of different companies and make informed decisions about where to invest their money.

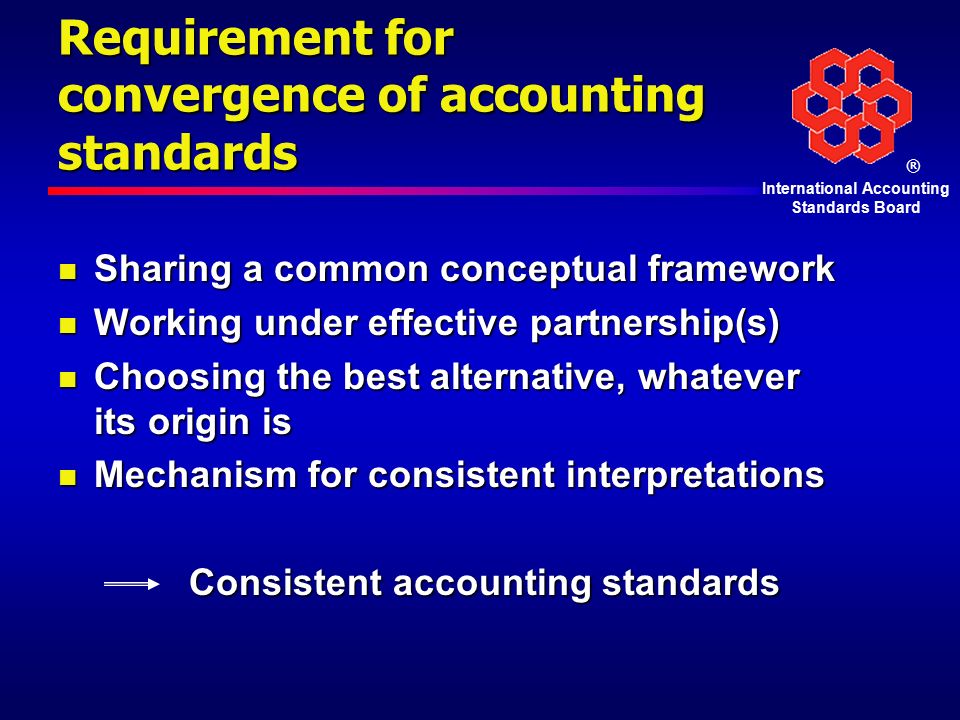

There are several organizations that have played a key role in the process of international convergence of accounting standards. One of the most influential of these is the International Accounting Standards Board (IASB), which is responsible for developing and issuing the International Financial Reporting Standards (IFRS). These standards are used by more than 120 countries around the world, and are recognized as the most widely adopted set of accounting standards in the world.

Another important organization in this process is the Financial Accounting Standards Board (FASB) in the United States. While the FASB has its own set of accounting standards (known as Generally Accepted Accounting Principles, or GAAP), it has also been actively involved in the process of international convergence. In recent years, the FASB has worked closely with the IASB to develop a common set of standards that can be used globally.

While the process of international convergence of accounting standards has made significant progress in recent years, it is still a work in progress. Some countries have fully adopted the IFRS, while others have chosen to adopt a modified version of the standards or to develop their own set of standards. Additionally, there are still differences in how different countries interpret and implement the standards, which can create challenges for companies that operate in multiple countries.

Despite these challenges, the process of international convergence of accounting standards is an important one, as it helps to improve the transparency and comparability of financial information, which is essential for the functioning of global financial markets. As the world becomes increasingly interconnected, it is likely that the process of international convergence will continue to be an important focus for accounting standard-setters and regulators.